When you deposit money into a bank, you want to know it’s safe. That’s where FDIC insurance coverage comes in. This government-backed protection ensures that even if your bank fails, your deposits remain secure up to certain limits. Understanding how FDIC insurance works, what it covers, and how to maximize your protection is essential for anyone managing savings or business funds.

The Origins of FDIC Protection

The Federal Deposit Insurance Corporation (FDIC) was created in 1933 during the Great Depression. At that time, thousands of banks collapsed, and depositors lost their life savings. FDIC insurance was designed to restore confidence in the banking system by guaranteeing deposits.

Since then, FDIC protection has become a cornerstone of financial stability in the United States.

What FDIC Insurance Coverage Includes

FDIC insurance coverage applies to most deposit accounts, such as:

- Checking accounts

- Savings accounts

- Certificates of deposit (CDs)

- Money market deposit accounts

It does not cover investments like stocks, bonds, mutual funds, or annuities, even if purchased through an FDIC-insured bank.

Coverage Limits Explained

Currently, FDIC guarantees up to $250,000 per depositor, per insured bank, per ownership category.

- A single account with $200,000 is fully insured.

- A joint account with $500,000 is insured because each co-owner is covered up to $250,000.

- Deposits spread across multiple banks are separately insured.

Ownership categories include single accounts, joint accounts, retirement accounts, and trust accounts. This structure allows depositors to maximize protection by diversifying account types.

Why FDIC Insurance Coverage Matters

Bank failures are rare today, but they still occur. FDIC protection ensures depositors don’t lose their money when a bank closes.

For example:

- During the 2008 financial crisis, several banks failed. Depositors at FDIC-insured institutions were protected.

- In recent years, regional banks facing liquidity issues triggered FDIC intervention, preventing panic and safeguarding deposits.

Without FDIC insurance, depositors would face uncertainty every time a bank struggled.

FDIC Insurance Coverage in Action

Example 1: Single Account

You have $200,000 in a checking account at Bank A.

- Fully insured because it’s below the $250,000 limit.

Example 2: Joint Account

You and your spouse have $500,000 in a joint savings account at Bank B.

- Each co-owner is insured up to $250,000.

- The entire $500,000 is protected.

Example 3: Multiple Banks

You have $250,000 in Bank A and $250,000 in Bank B.

- Both accounts are fully insured because coverage applies per bank.

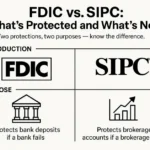

FDIC Insurance Coverage vs Other Protections

FDIC insurance is unique because it’s backed by the U.S. government. Other protections include:

- SIPC (Securities Investor Protection Corporation): Protects brokerage accounts, but not against investment losses.

- Private Insurance: Some banks offer additional deposit insurance, but FDIC remains the most reliable.

What Happens When a Bank Fails

When a bank fails:

- FDIC steps in as receiver.

- Depositors are paid back, usually within days.

- Accounts may be transferred to another bank.

This swift action prevents financial disruption for depositors.

Maximizing FDIC Insurance Coverage

To ensure full protection:

- Spread deposits across multiple FDIC-insured banks.

- Use different ownership categories (single, joint, trust).

- Confirm your bank is FDIC-insured (look for the FDIC logo or check the FDIC website).

What People Commonly Misunderstand

There are persistent myths around FDIC insurance coverage:

- “My investments are insured.” False. FDIC does not cover stocks, bonds, mutual funds, or crypto.

- “FDIC covers unlimited amounts.” False. The cap is $250,000 per depositor, per bank, per ownership category.

- “My fintech app is FDIC-insured.” Misleading. Apps themselves are not insured; only the partner banks are.

- “Joint accounts double coverage automatically.” True, but only if both owners are listed. If one spouse isn’t named, the account may only be insured up to $250,000.

- “FDIC takes months to pay.” False. In most cases, depositors regain access to insured funds within a few days.

What Happens in Less Obvious Cases

FDIC protection sounds straightforward, but in practice there are tricky scenarios:

- Trust Accounts with Multiple Beneficiaries: A revocable trust with five beneficiaries can be insured up to $1.25 million at one bank ($250,000 per beneficiary). Many depositors don’t realize this multiplier effect exists.

- Business Accounts: A small business with payroll funds of $400,000 in a single checking account is only insured up to $250,000. If the business splits funds across two FDIC-insured banks, the full amount is protected.

- Bank Mergers: If Bank A and Bank B merge, deposits that were separately insured may suddenly be combined under one FDIC certificate. Customers sometimes lose coverage unless they restructure accounts.

- Temporary High Balances: After selling a house, you might have $600,000 in your account. FDIC insurance only covers $250,000 unless you spread the funds across institutions or categories.

Practical Ways to Stay Protected Under FDIC Insurance

To make the most of FDIC protection:

- Regularly review your accounts.

- Understand ownership categories.

- Stay informed about your bank’s status.

Global Comparisons

Other countries have similar deposit insurance systems:

- Canada has CDIC (Canada Deposit Insurance Corporation).

- UK has FSCS (Financial Services Compensation Scheme).

FDIC insurance coverage sets the standard worldwide.

Future Challenges

As banking evolves, FDIC faces new challenges:

- Digital currencies and crypto assets are not covered.

- Rising deposit amounts may require higher coverage limits.

- Global interconnectedness increases systemic risks.

Conclusion

FDIC insurance coverage is one of the most powerful protections for depositors. It ensures that your money is safe even if your bank fails. By understanding how it works, you can maximize your coverage, reduce risk, and enjoy peace of mind.

Key Takeaways

- FDIC insurance coverage protects deposits up to $250,000 per depositor, per bank, per ownership category.

- It covers checking, savings, CDs, and money market deposit accounts.

- It does not cover investments like stocks or crypto.

- Depositors can maximize coverage by using multiple banks and ownership categories.

- FDIC protection stabilizes the financial system and prevents bank runs.

Frequently Asked Questions

Are fintech apps and online banks covered by FDIC insurance?

FDIC insurance applies only if your money is held at an FDIC-insured bank. Many fintech apps partner with insured banks, but coverage depends on how the funds are stored and whether the app properly records your ownership. Always check the app’s disclosures to confirm FDIC coverage and the name of the partner bank.

What types of accounts are not covered by FDIC insurance?

FDIC insurance does not cover investments such as stocks, bonds, mutual funds, cryptocurrencies, annuities, or life insurance—even if they are purchased through an insured bank. Safe-deposit box contents are also not insured.

How can I check whether my bank or app is FDIC insured?

You can verify FDIC insurance by searching the FDIC’s official BankFind tool or by checking whether the bank displays the FDIC logo. For fintech apps, confirm both the partner bank’s insured status and how your funds are recorded.

Video Explanation by FDIC

Explore more articles